by Mike Shallanberger | Jan 15, 2019

“I view my primary job as strengthening our talent pool.” — Jack Welch

No amount of coaching can offset poor hiring decisions, and the cost of a bad hire is estimated conservatively to be at least two or three times an employee’s annual salary plus thousands of dollars in lost opportunity cost for sales not made and for customers lost. The society for Human Resource Management (SHRM) estimates a hiring mistake could even cost as much as five times the employee’s annual salary.

The new reality in our industry is that we now have to get more sales from fewer people. It’s particularly crucial that you identify strategically critical jobs, and then invest your time and resources disproportionately to ensure that the right people, doing the right things, are in these positions. The more complex the sales or sales leadership task is, the bigger the performance gap between top and low performers.

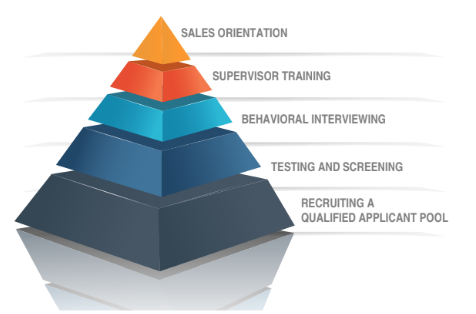

That’s why Schneider Sales Management has developed a five dimensional hiring process. It works like a funnel that starts with the hiring managers and ends with satisfied, productive employees who meet (or beat!) sales performance standards.

Starting at the bottom of the funnel and working up, the first stage of the five dimensional hiring process is continuous talent recruiting. To be successful at strengthening the sales staff, hiring managers need to recruit continuously, tailor their recruiting to target applicants (or, “fish where the fish are,” as the old adage goes), and build the applicant pool by selling the opportunity of working at your organization.

In the testing and screening stage of this process, hiring managers need to find the right tools to prescreen applicants quickly for fit to their sales roles, and find effective ways to maximize the impact of the first in-person interview. Once candidates have been tested and screened, they can be interviewed based on their personality traits and behaviors.

These behavioral interviews will focus interviews on required behavior and results and adhere to a structured interview guide. The interviewees’ answers during behavioral interviews should be compared to and measured against the job requirements, not to other candidates’ responses. There is a right and wrong way to interview, so make sure you’re adhering to legal standards during each candidate conversation.

After the selection process comes two of the most vital stages—stages that many financial institutions mistakenly consider separate from the hiring process.

Each new hire needs a strong sales orientation program and a conditional job offer with an onboarding plan in place. It’s important to outline expectations for new salespeople early on to avoid any confusion about the job role and to get them out of the starting blocks strong.

These tools together create hiring that can give banks and credit unions the quantum leap in performance that they need. Hiring mistakes are too expensive to make, and changing your hiring behaviors is an investment that your organization can make to improve your overall culture and revenue.

We’re the only firm in the industry that can help you put in place a process with these five dimensions. For more information on our support for hiring and HR managers, call us today at 303-221-4511.

by James Schneider | Dec 13, 2018

The moment when a hiring manager shakes the hand of a new hire and welcomes him or her to the team is a hopeful one on both sides of the agreement. Salespeople begin with great hope that they’ll have the staff support and goal structure to help customers and the ability to earn a living while they’re at it. Hiring managers hope that the hire will be a good fit— that they won’t have to interview again for the same role due to employee turnover.

Salespeople who join an organization may not succeed for several reasons. The failure to succeed in selling may show up in sales conversations — the salesperson could “dump” product features on customers, give price or product details too early in the sale, or end conversations with no next step commitment. This ends up in low conversion rates, low performance, and low sales numbers.

One of the main reasons that salespeople fail is because they have been hired for a sales role for which they are not the right fit. We know that different selling roles require different competencies. The industry research we conducted with the University of Colorado at Denver Business School proves that there are actually five primary selling roles in banks and credit unions, each requiring a different set of competencies that drive high performance.

The five roles are SERVICE SELLING (think “teller”), CONSULTATIVE SELLING (think “personal banker”), COMPETITIVE SELLING (think “commissioned mortgage originator” or “business development officer”), COMPLEX SELLING (think “commercial lender”), and SALES SUPERVISION (think “branch manager” or “sales manager”).

Two additional roles, FRONTLINE SUPERVISION (think “teller supervisor”) and ENGAGEMENT SELLING (think “universal banker”) are subsets of these primary roles.

For hiring managers, it’s vital to get an assessment that can evaluate the strengths and weaknesses of each candidate for the specific type of selling that they’ll be doing every day. These hiring managers need to look at sales capability as a series of skills that can be improved, not a natural-born talent or personality fit.

The most important first step for financial industry hiring managers is to screen candidates using the Optimum Performance Profile™ sales assessment. This cutting-edge hiring tool is based on the results of our industry research, and it can predict a salesperson’s performance with a much higher degree of accuracy than a standard interview.

Learn more about these assessments today to improve the success rates of your bank or credit union’s new hires, and get in touch for a free trial so you can increase revenue in 2019.

by Mike Shallanberger | Oct 2, 2018

Give a child a cookie and you can get him to take a nap or clean his room. Behavior can definitely be influenced by rewards—something we never outgrow. But do sales incentives work? Unfortunately, bankers typically misuse incentive pay by choosing the wrong behavior to reward or by rewarding everyone regardless of discretionary effort. In most cases, results under incentive plans are the same as if we had simply managed and coached employees better…

Banks and credit unions fund sales incentive plans to get employees to do more. But more of what? Doing more of some activities and some sales production is actually counter-productive. Just ask any mortgage bankers who lost their shirt compensating lenders for overselling low-down payment loans, or branch managers who are seeing dozens of investment referral attempts with no closed business.

In some selling roles, bank incentive programs may not be cost effective and aren’t even terribly motivating. When we ask top producing tellers why they are making 100 referrals a month when most tellers only make 1 or 2, the answer isn’t the extra $5 they make on each referral. The answer is almost always that making 100 referrals per month will get them noticed, and if they get noticed they can get promoted.

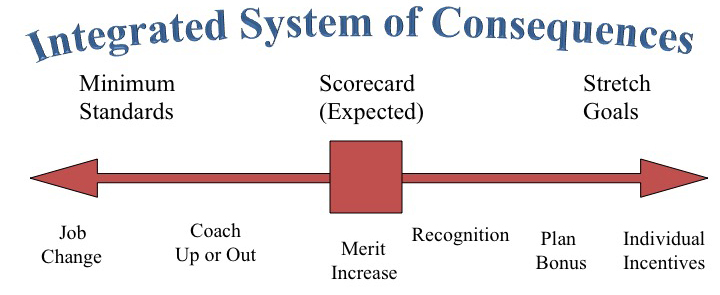

Sales compensation is driven by employee scorecards and goals. If the scorecards are balanced or weighted properly, you’ll pay for the wrong results. If the goals are off, you either overcompensate employees or demotivate them. Surprisingly, we find that most banks and credit unions overpay their employees with incentive dollars by trying to pay everyone something instead of paying their best contributors more for the results that matter most.

To realize maximum value for your incentive payouts, pay only for sales above a goal level achievable by training and good supervision alone. Pay for behavior and outcomes that are profitable, within the employee’s control and associated directly with discretionary effort. Finally, pay disproportionately to top producers and supervisors who drive most of your production. At most financial institutions, 50% or more of incentive dollars go to average performers.

To encourage sales leaders to coach, pay them for achieving a specified percentage of employees meeting goals so they can’t rely on one or two employees to carry their team without coaching everyone. One of the most successful and sustainable incentive programs we’ve seen paid regional managers on two factors – the percentage of employees meeting and exceeding goal and the percentage of employees who met the requirements to be promoted to the next level.

Sign up for The Schneider Report below for free tips on how to increase your revenue, hire employees who can sell, and increase customer satisfaction.

by Mike Shallanberger | Oct 1, 2018

Why is it so important that banks and credit unions hire better salespeople, starting today? U.S. bank branches are closing down at record rates. The Wall Street Journal reported in February 2018, “The number of branches in the U.S. shrank by more than 1,700 in the 12 months ended in June 2017, the biggest decline on record, according to a Wall Street Journal analysis of federal data.”

Why are so many banks closing?

One reason is that more people are using online banking apps and tools, which leads to fewer visits to local branches. This leads to fewer face-to-face opportunities to sell.

Fewer people are answering their phones or calling to talk with their bank or credit union representatives about their savings, checking, and investment accounts.

This means that banks need to create more sales, and more opportunities for interactions, with fewer points of contact.

With growth no longer a priority, many organizations eliminated the crucial sales development manager role and cut staffing and funding for sales support. More employees were forced into jobs requiring multiple selling, coaching and/or operations roles, many of which weren’t a good fit for their talents, and the time allotted for actual selling was reduced.

With fewer employees and fewer opportunities to sell, every employee, needs to be an excellent salesperson in addition to meeting the other requirements of their job. For Human Resources professionals, hiring customer-facing employees who are great sellers is an enormous challenge.

How can Human Resources professionals make sure that each new bank or credit union hire has the potential to bring in more revenue?

Schneider Sales Management has a forty-year track record of helping clients increase net income per employee at a rate three times faster than the industry norm. We’ve done extensive research into the best practices of top performing salespeople and have studied how banks and credit unions can make each customer or member interaction work to increase revenue and improve satisfaction and loyalty.

Based on our research, here are five ways you can hire better salespeople, starting TODAY.

- Create the Right Sales Goals. Challenging sales goals work as a motivational tool for the simple reason that salespeople work harder and longer to achieve them. At most banks and credit unions sales goals are set at the top and divided among business units and branches based on recent history and divided among individual salespeople equally by job role without negotiation. Typically, every salesperson in a job role like personal banker will have the same goals regardless of experience, competence or sales opportunity. For decades, we’ve recommended to our clients that they implement a simple goal setting process based on 90-day action plans negotiated between individual salespeople and their supervisor. Each plan includes 3-5 annual goals, 3-5 objectives for the quarter, activities and strategies to accomplish the short-term objectives, and the selling behavior the employee will work to improve.

- Conduct 90-Day Onboarding. When you hire salespeople you’re making an investment, and you need an immediate return on that investment given the industry’s high employee turnover rate. You never want an employee to leave because he or she didn’t feel prepared to meet your expectations for sales. The right way to do sales orientation is to state your expectations for the first 90 days in terms of learning, preferred behavior and sales production, to invest in product training and sales training immediately so employees know how to succeed, and to require new employees to test out on various aspects of product knowledge and preferred behavior throughout their orientation.

- Incentivize properly. Sales compensation is driven by employee scorecards and goals. If the scorecards are off, you pay for the wrong results. If the goals are off, you either overcompensate employees or demotivate them. Surprisingly, we find that most banks and credit unions overpay their employees with incentive dollars by trying to pay everyone something instead of paying their best contributors more for the results that matter most.To create maximum value for your incentive payouts for any job role pay only for sales above a goal level achievable by training and good supervision alone, pay for behavior and outcomes that are profitable, within the employee’s control and associated directly with discretionary effort, and pay compensation disproportionately to top producers and supervisors who drive most of your production.

- Hire for the right selling role. Simply put, different selling roles require different competencies. Our industry research identified five distinct selling roles in banks and credit unions, each requiring a different set of competencies that drive high performance. The five roles are SERVICE SELLING (think teller), CONSULTATIVE SELLING (think personal banker), COMPETITIVE SELLING (think commissioned mortgage originator or business development officer), COMPLEX SELLING (think commercial lender), and SALES SUPERVISION (think branch manager or sales manager). Two additional roles, FRONTLINE SUPERVISION (think teller supervisor) and ENGAGEMENT SELLING (think universal banker) are subsets of these primary roles.

- Assess bankers’ sales potential before you hire. The difference in sales production between top sales producers and average or low producing salespeople in banks and credit unions is staggering. Hiring employees who can sell is vital to increasing revenue. Our groundbreaking national research with the University of Colorado at Denver Business School concluded that top producers outsell average producers two-to-one and outsell low producers ten-to-one. This is true for every selling role from teller and personal banker to commercial lender and mortgage originator.

For HR Managers, the Optimum Performance Profile™ is a groundbreaking tool to assess and profile candidates for their sales aptitude. Learn more about the tool and shift your bank or credit union’s culture to one that transforms each contact, each lead, and each conversation revenue.